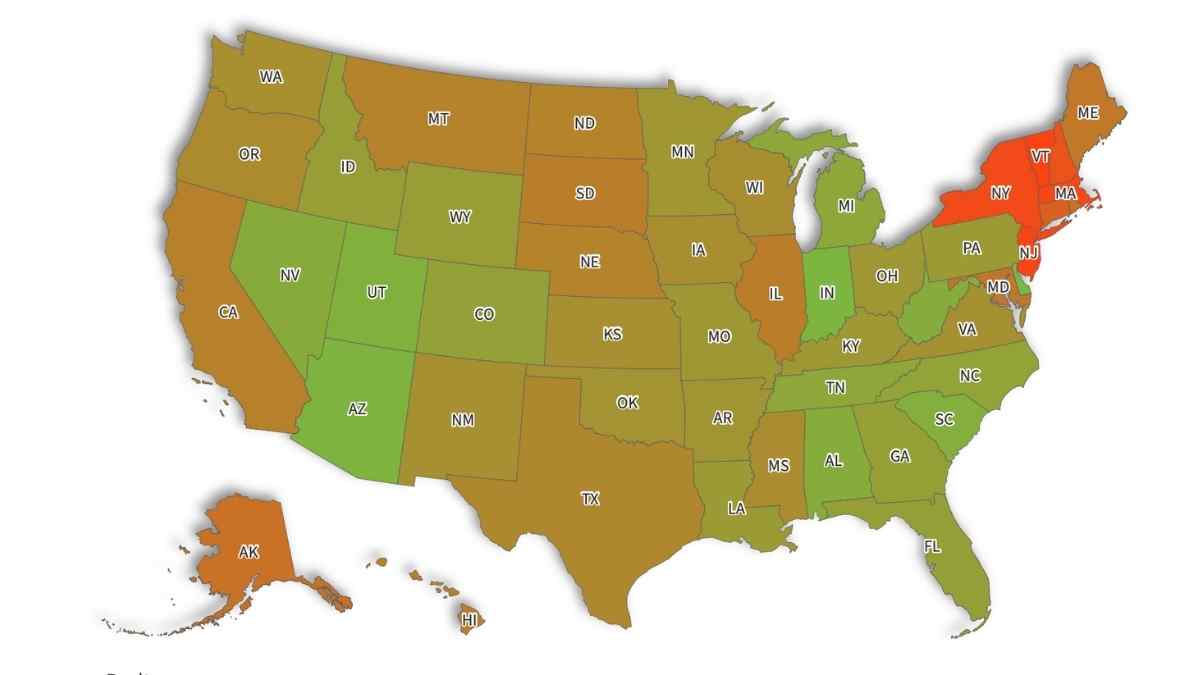

Social Security remains the main source of income for millions of American retirees, but it is stretching less and less. According to a new analysis, living only on this benefit is now realistically possible in just 10 states for homeowners who have already paid off their mortgage.

The study, conducted by real estate portal Realtor.com and reported by Newsweek, compares the median Social Security check in each state with the basic cost of living for people over 65. It concludes that in most of the country, benefits do not cover essential expenses and force retirees to top up their income with savings, part-time work or other forms of support.

To run the numbers, analysts used the Elder Economic Security Standard Index, an indicator that estimates how much an older adult needs to cover housing, food, health care, transportation and other basic costs.

Over the past five years, the cost of homeownership has risen by about 26%, driven less by mortgage payments than by taxes, insurance, utilities and maintenance. Even with a paid-off home, the average retiree faces an annual gap of about $2,762, roughly $230 a month.

This shortfall comes at a time when Social Security plays a decisive role in seniors’ budgets. According to data from The Senior Citizens League (TSCL), almost three-quarters of older Americans rely on Social Security for more than half their income, and for 39% it is their only source of money. TSCL estimates that around 22 million people live exclusively on their monthly benefit.

The factor that most determines whether the check lasts until the end of the month is housing. The costs of food, health care and transportation are relatively similar from one state to another, but the price of keeping a roof over one’s head varies widely. In the 10 states where Social Security is enough, average housing costs are about $510 a month.

Elsewhere, that figure climbs to almost $933, and in several East Coast states it exceeds $1,000. As a result, housing rises from 27% of a retiree’s budget in “surplus” states to 32% in deficit states.

Where Social Security Still Covers Basic Living Costs

Among the places where Social Security goes furthest, Delaware stands out. It tops the list with an annual surplus of $1,764 for homeowners without a mortgage. There, the median monthly benefit is around $2,139, while basic monthly living costs are estimated at about $1,992.

Next is Indiana, where retirees enjoy an annual cushion of $1,392, thanks to a typical benefit of $2,016 and relatively modest housing costs of about $504 a month.

Arizona (with an annual surplus of $1,224) and Utah ($888) also remain in positive territory. In both states, median benefits are close to $2,000, and housing costs run at about $530 a month.

South Carolina rounds out the top group, with retirees ending the year, on average, about $828 ahead of their basic expenses.

According to the analysis, other states where Social Security alone is enough to cover needs for those without a mortgage are West Virginia (+ $660 a year), Alabama (+ $576), Nevada (+ $432), Tennessee (+ $156) and Michigan (+ $132). The margins are slim, but these states still offer a bit more breathing room for unexpected costs.

States Where Retirees Face the Largest Gaps

The picture changes completely in the states facing the biggest challenges. Vermont ranks as the worst off, with an annual deficit of $8,088: monthly expenses come to about $2,628, compared with a median benefit of $1,954.

Close behind are New Jersey (–$7,512 a year) and Massachusetts (–$7,345), where housing bills of $1,304 and $1,007 a month, respectively, account for much of the gap.

Also among the hardest places to live on Social Security alone are New York (–$7,248) and New Hampshire (–$6,564).

The authors of the report note that in these states, relying solely on Social Security forces retirees to cut back on basic spending or look for extra income, something especially difficult at advanced ages.

In the background, the study revives the debate over the economic sustainability of retirement in the United States and how much of the burden should fall on private savings and public policy to keep millions of older adults from sliding into poverty.